Everyone has a desire to have their own house and also consider it to be their best possession. Is it better to buy a house or rent one? is a subject matter for another discussion. Currently, as the financial institutions are offering great interest rates on Housing Loan. Therefore, we will discuss about buying a house through a loan from financial institutions and the following issues will be addressed.

Issues:

- What are the documents required for availing a Housing Loan from a financial institution?

- What will be the most suitable tenure of loan for the borrowers?

- Is it beneficial/savings in interest for the borrowers if they prepay loans whenever they have excess funds?

- Is it the right time to avail of a housing loan?

What are the documents required for availing a Housing Loan?

Identity-related:

- Copies of citizenships of people involved along with their 3 generation details (borrowers, property owner(s), guarantors, spouses, people whose income has been considered usually made co-borrowers, major legal heirs in the family)

- Recent passport size photographs of the people involved as mentioned above.

- Relationship certificate

Property related:

- Copy of land ownership certificate (LOC)

- Copy of land and/building tax receipt

- Four boundaries certificate (Original)

- Trace Naksha and Blueprint (Computer print is issued at present) (Original) (Bank has to issue a letter to Napi for the map print. the prospective borrowers will pay the cost and the bank staff will collect the computer print)

- Building’s Blueprint, Building Construction permission and Building construction completion certificate in case of already built building)

Income-related:

- Income certificate from the respective employers certifying the income, rent agreements or Audited Financial statements.

- Bank statement to support the income.

- Tax receipts

Note: Required documents for loans may slightly differ among financial institutions

What will be the most suitable tenure of loans for the borrowers?

Let’s consider an example:

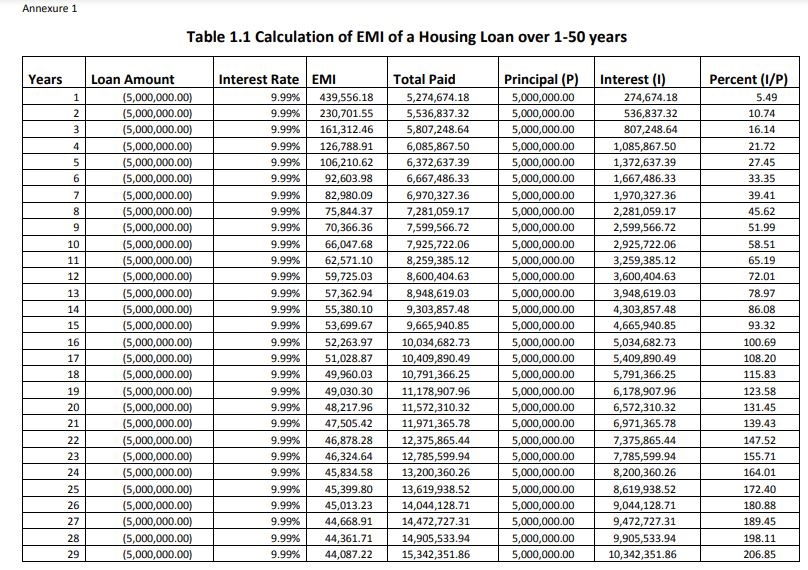

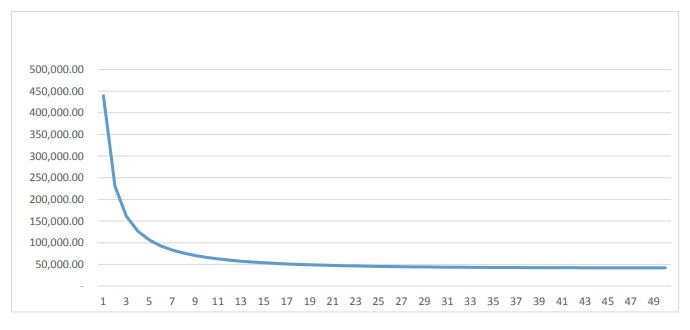

We have calculated the proposed EMI for Home Loan of Rs.50.00 lacs at 9.99% per annum from year 1 to 50 which has been shown in Annexure 1. The EMI from the calculation has been plotted in the graph below.

Fig: 1.1 Proposed EMI over Tenure of Loan

From the Fig1.1, we see that from year 1 to year 9, the proposed EMI of loan has reduced drastically with the increase in tenure of loan and decreased slightly up to 15 -17 years. However, after that, the proposed EMI has decreased insignificantly regardless of increase in the tenure of the loan. This shows that after certain duration, there is no much benefit to the customer by increasing the tenure of the loan, because the difference in proposed EMI to be paid is very low. It would be rather wise to stick to lowest tenure of loan possible and pay a bit larger sum of money as EMI to pay off the loan as soon as possible. There are two things that one should also consider: (i) one can also pay low EMI by opting for longer tenure of loan and later prepaying the loan as soon as possible. (ii) there are also restriction from the NRB regarding how much EMI can a bank deduct like 50% of gross income and some restrictions from the bank like uncommitted monthly income should be certain time of EMI etc.

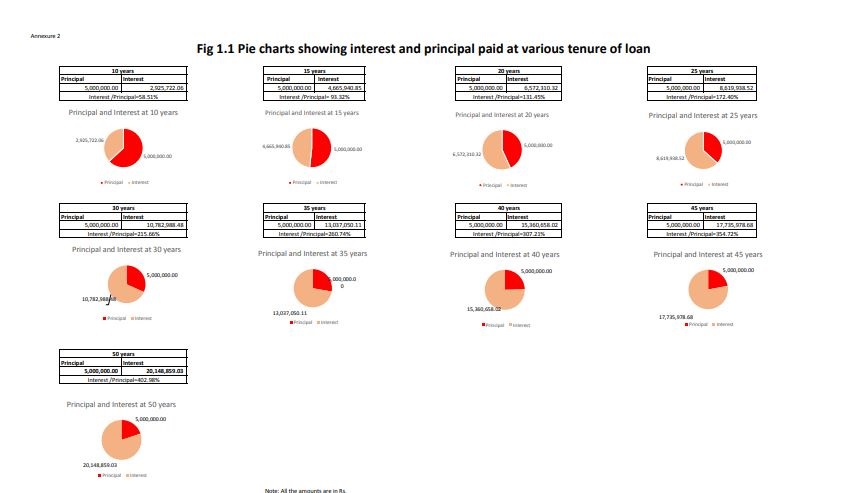

Mr. James has to pay more than the principal when he borrows money from the bank. But how much more? Let’s find out by learning more from our example discussed above:

From the pie charts shown Annexure 2, we can see that after 15 years’ tenure of loan, he pays more than what he borrows. What is ridiculous is when he borrows money for 50 years, he pays 402.98% i.e. more than 4 times in interest only on what he has actually borrowed. So, let’s be informed and make our decisions likewise.

Conclusion: The most suitable tenure of the loan is 10-15 years. However, when the quantum of loan is decreased i.e. Rs.10.00 lacs, the suitable tenure of the loan will shift towards the left and if the loan is increased to Rs.70.00 lacs, the suitable tenure of the loan will shift towards the right.

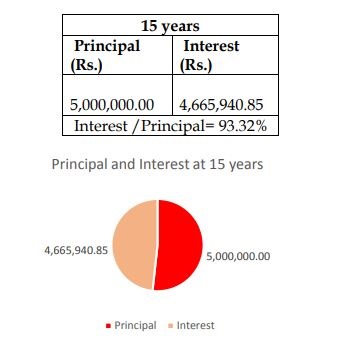

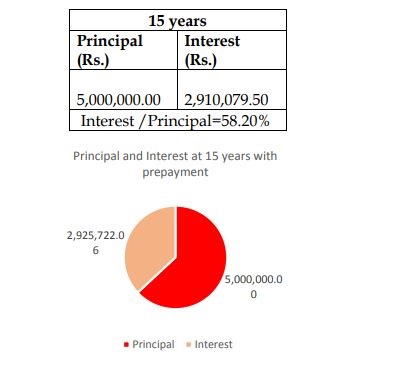

Will it be any beneficial/savings in interest if Mr. Hari Bahadur prepays loan whenever he has excess funds?

We will assume that Mr. Hari Bahadur has opted for a Housing loan of Rs.50.00 lacs for the period of 15 years @9.99%. In doing so, his EMI is Rs. 53,699.67. Over 15 years, he pays Rs.96.66 lacs to repay his loan completely out of which Rs.50.00 lacs is principal and Rs.46.66 lacs is his interest. The ratio of his interest to the principal is 93.32%. He pays as per the following plan:

Now, we will also assume that he receives Rs. 100,000.00 additional incomes (from a bonus, agriculture, an income of spouse, rent, etc.) per year and decides to put the money towards the reduction of Housing Loan. We will now see how much saving he is making on payment of interest by doing so.

We can see from the above calculations that when James contributed an additional Rs.1.00 lacs per year towards the reduction of the housing loan, his EMI has remained the same however he only paid Rs.29.26 lacs as interest and the duration of the loan was also reduced from 180 months (15 years) to 114 months (9.50 years~ 10 years). By making an additional contribution, he was able to save Rs.17.40 lacs in interest. (i.e. 37.29% of total interest paid in loans without prepayment).

Conclusion: It is always better to prepay the term loans whenever one has excess funds.

Is it the right time to avail a housing loan?

Covid 19 has mostly impacted service sectors and also some of the industries. Due to this people have lost their jobs and income. This has resulted in a decrease in the purchasing capacity of the people. Due to this, people have started saving money and buying only the essentials. People have abandoned all the purchases like house, car etc. As there is no demand for loans in the bank, the banks have also reduced interest rates in most of the loans. Are these interest rate cut permanent? The answer is no. Once the pandemic is over, the economy will bounce back, the demand for loans will increase and the interest rates on loans will certainly go up.

As the purchasing capacity of people has decreased, the demand for real estate has also decreased. There are more sellers of properties in the market than buyers. This has resulted in a decrease in the market value of the properties. Therefore, before buying a house, Mr. James should consider the following factors:

- Will COVID 19 pandemic be contained very soon or will it become worse? If it· became worse, the value of properties will further decline.

- The housing loan is generally for more than ten years. Will his job and income· remain intact for the same period? If his job is gone, how is he planning to repay his EMIs?

- Though the bank’s interest has decreased now, it will increase once the economy gets momentum. If the interest rate rises significantly, will he be able to continue to pay the EMIs of his Housing loan?

- The banks themselves will not finance employees of badly hit sectors such as travel and tourism, hotels etc.

Conclusion: If you sure about your job and income and the bank is also convinced regarding the same, you may buy a post-earthquake already constructed building if you get really good deals in the properties. It will be nice if the building also generates some income. However, if you are planning to get a house constructed through a bank loan you will face many difficulties. Though the prices of the raw materials of the construction have gone down and if you have already got your permissions ready, it is very difficult for you to get labor force for the construction leading to delays and an increase in the cost of construction.

*****************************************

(The author is post graduate in finance and working in an ‘A’ class financial institution for the last twelve years. The views expressed in the article are his own. The author may be contacted at baibhav.kharel@gmail.com)