Moreover, the NPL may further increase due to ongoing liquidity crisis and high-interest rates.

In the present context, the banks have been unable to recover loans from borrowers. The loan default fueled by a spike in interest rates, economic recession and the aftermath of COVID-19 has skyrocketed the loan default rates of the banks.

A few weeks back, the Federation of Nepalese Chamber of Commerce and Industries (FNCCI) had projected that the NPL of banks may go beyond 5 percent. Shekhar Golchha, President of FNCCI, in a press conference, said that a study conducted had projected that the NPL of banks may increase above 5 percent if the economic situation os the country does not improve.

Apparently, the projection made by FNCCI is becoming reality. The NPL of banks has doubled in the last year which does not seem to slow down any time soon.

“Generally, when the interest rates rise, loan recovery slows down,” said a banker. “However, the current scenario is due to the current economic condition. The phase may be extended for quite a sometime,” he added.

Moreover, the ongoing rowdy activities against banks may provoke many to default payment which may further escalate the situation.

The NPL may heighten in the coming quarter compared to the second quarter. The extended period given during COVID-19 has ended but the borrowers have not repaid the loan.

Nepal Rastra Bank (NRB) had given extra time to incapable borrowers to repay loans. The deadline ended long ago but the borrowers are repeatedly saying of being unable to pay the loan. Currently, many borrowers have stopped paying the loans which have increased the NPL.

At the same time, the decline in cash flow in the market because of restricted loan extensions by the banks will also increase the NPL. According to experts, a decline in cash flow also brings down the repayment capacity of borrowers.

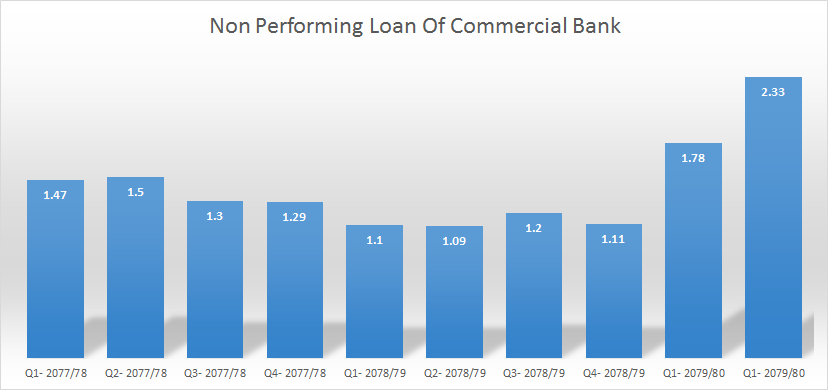

Commercial banks that had logged NPL of 1.1 percent in the first quarter of the current FY logged NPL of 1.78 percent in the corresponding period of the current FY. It further increased to 2.33 percent in the second quarter. It is considered risky if the NPL reaches above 5 percent in the banking sector. NRB takes action against such banks whose NPL goes beyond 5 percent.

Sometimes ago, commercial banks raised deposit interest rates which consequently increased loan interest rates. There is a liquidity crisis in the market, above that, the tightening of working capital by NRB has squeezed the loan repayment capacity of people. It has worsened the loan recovery of banks.

Moreover, many business federations have openly said that they can not repay until the central bank provides subsidies.

The banks have also tried to auction collateral to recover loans, however, they failed to sell those assets even in multiple attempts due to which their non-banking assets are increasing.

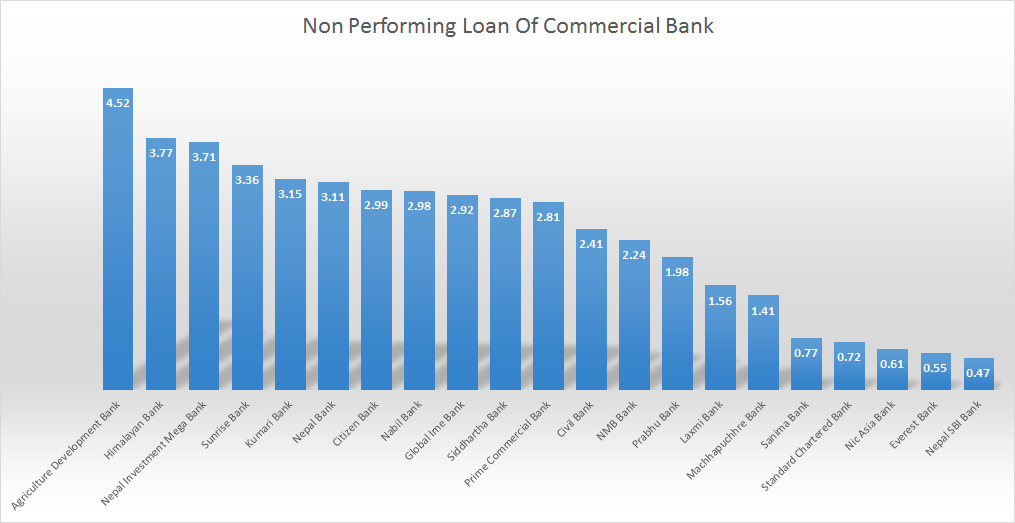

Half a dozen banks have NPL above 3 percent

As per the second quarter report, half a dozen banks have NPL above 3 percent.

Government-owned Agriculture Development Bank logged the highest NPL of 4.52 percent. There is a high possibility that the bank will face the music if it does not bring NPL down in the coming days.

In the second quarter, NPL of Agriculture Development Bank, Himalayan Bank, Nepal Investment Mega Bank, Sunrise Bank and Kumari Bank exceeded 3 percent.

Out of all, five commercial banks have NPL below 1 percent. Nepal SBI Bank has the least 0.47 percent NPL followed by Everest Bank with 0.55 percent, NIC Asia Bank with 0.61 percent, Standard Chartered Bank with 0.72 percent and Sanima Bank with NPL of 0.77 percent.

(Note: Himalayan Bank and Civil Bank started joint transactions after the second quarter, thus, their data has been kept separately in the table)