When borrowers default and public auctions fail to attract buyers, banks have no choice but to absorb the properties onto their own balance sheets. Economists warn that locking up billions in illiquid real estate poses a dual threat to the banking sector, directly squeezing profitability and choking liquidity management.

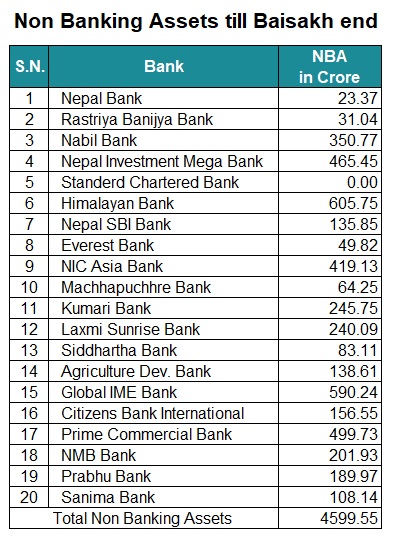

The impact of the crisis is unevenly distributed across Nepal's 20 commercial banks. While aggressive private lenders are heavily weighed down by foreclosed properties, state-owned institutions and conservative players remain relatively insulated.

Standard Chartered Bank Nepal has completely avoided the NBA quagmire. By eschewing aggressive credit expansion and strictly prioritizing high-quality, safe investments, the bank maintained a flawless asset slate of zero NBAs. In contrast, state-owned entities like Rastriya Banijya Bank and Nepal Bank also showcased comfortable bad-loan positions compared to their

The primary function of any bank is to mobilize capital and generate interest income. However, having billions frozen in illiquid real estate severely restricts a bank's capacity to issue new loans and drastically shrinks distributable profits.

Bankers point out that this crisis is a direct symptom of broader economic paralysis inclusing a frozen real estate market preventing property liquidation, a massive slowdown in the construction sector and subdued consumer and business market activity.

While Nepal Rastra Bank (the central bank) has been ramping up pressure on financial institutions to clear out bad loans and offload these non-banking assets, market realities make immediate cash conversion nearly impossible.

To prevent the financial system from shrinking further, the government and the central bank are moving toward a structural intervention: the establishment of a specialized National Wealth Management Company. Initially conceptualized in Nepal Rastra Bank’s Monetary Policy through a draft of the 'Asset Management Act', the initiative mimics global "bad bank" models. This state-backed asset management entity will be legally empowered to buy up dead assets directly from commercial banks. This will clean up bank balance sheets and allow lenders to refocus entirely on core banking operations.

While the government assures that the company is actively being structured as promised in the federal budget, sluggish legislative processes and structural delays mean that commercial banks will have to continue carrying the heavy Rs 46 billion burden for the foreseeable future.