We also developed a simple framework of looking at the risk and returns as if a mutual fund was providing a index product. If you haven’t checked out that article, I strongly encourage you to first read that. You can find it in here. This is because what follows now is a kind of sequel to the first one, if you will !

Starting with this article, we shall be looking closely at different sectors in Nepal stock market. As you might already know, the Nepal Stock Market has different sectors such as Banking, Development Banks, Insurance, Microfinance etc. Hence, not surprisingly, there are sub-indices that reflect the performance of these sectors. Today, we shall be checking out some the major descriptive statistical measures with regards to the Banking sector. The process and framework will be very similar to what we talked about in the first article. So, let start….!

(And just for your information, I won’t be explaining every statistical measure like I did in the previous article because it will start getting redundant)

Banking

Perhaps the major sector in Nepal, the commercial banks dominate the Nepalese capital markets. In everything, from volume to transaction to total capital of the industry, it comes out at the top. But how well has it fared in generating returns for the investors?

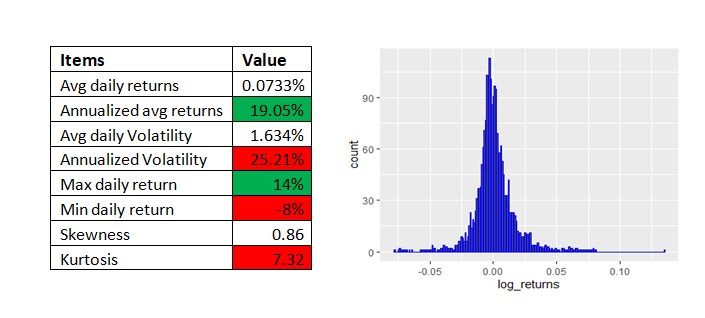

Now, as you can see, the annualized returns look pretty good. But as its often said in finance industry that “there is no free lunch”, it comes with a cost and that is the volatility. Just look at the annual volatility of 25%. Imagine your portfolio losing 25 % in a year. How’d that feel? Another bit of lesson that I want to share with you is with regards to the performance and risks of sub-indices VS the total market index. Check out the annual returns and volatility in the above table and compare it with that of NEPSE’s (You can find this in the previous article). What you will find is that the commercial banks have done slightly better by generating annual returns of 19.05 % compared to NEPSE’s 18.36 %. However, it’s not all roses and sunshine here. That’s because if you look at the risk category, commercial banks as on aggregate are more volatile than NEPSE by around 5 percentage points.

Now, think about it..! Why did that happen? Why commercial banks exhibit more risky characteristics compared to the total market index? Well, the answer is fairly straight forward. There are around maybe 300 companies in NEPSE whereas there are just about 27 commercial banks. Now, you might ask, So, what …? Good question…! That 300 companies which forms the overall NEPSE index are different types of companies operating in different sectors and market environment. Hence, this brings out the concept of diversification. I am going to talk about diversification in detail in a future article. But for now, what I am trying to say here is that the very fact that NEPSE has all these different types companies that are operating in different situations and circumstances from each other makes NEPSE as a whole less risky than just the commercial banks. In other words, the risk is diversified away. That my friends, is one of the founding principles in Modern Portfolio Theory.

Another interesting thing to talk here is the excess kurtosis. There’s a massive kurtosis of 7.32. The reason for such a large value is because of an outlier value. If you look at the histogram, you will see the right tail being stretch far. So, essentially what is happening here is that one outlier value is pulling all the other values towards it. Now again, you might be asking, how does it relate to my portfolio risk return trade-offs? The answer would be to be cautious of such security which has such excess kurtosis.In this case, the kurtosis emerged due to the extreme positive return and nobody complains when there is upward risk, right..?! However, if it was on the negative side, then it would be a problem.

Bivek Neupane is a MSc. Finance and Economics student. He is also a CFA candidate. He is specializing in quantitative finance and research. His other interests include Portfolio optimization, Behavioral finance, Alternative asset management etc. Connect with him via LinkedIn (https://www.linkedin.com/in/bivek-neupane-6478b9177/). Check out his GitHub page if you want to access the R modules (https://github.com/biv-neupane7/NEPSE-stat-analysis).